FREQUENTLY ASKED QUESTIONS

FAQs provide quick answers to common questions, improving customer experience and reducing support requests

FAQ

FAQs provide quick answers to common questions, improving customer experience and reducing support requests

Frequently Asked Questions

Frequently Asked Questions

📜 ESTATE PLANNING FAQ - COMMON WAYS TO HOLD TITLE TO REAL PROPERTY IN THE U.S.

1 . The most common ways to hold title to real property in the U.S., especially when two or more people are involved:

1️⃣ Sole Ownership- Who uses it: Single individual or entity (such as a corporation or trust).

- Effect: Full control by the owner; transfers by will or trust upon death.

- Best for: Single buyers, investors, or trusts.

- Key Feature: If one owner dies, their share automatically passes to the surviving owner(s).

- Must Have:

- Equal ownership shares

- All owners must acquire title at the same time

- Same title document

- Equal rights of possession

- Rights: No will needed for survivor to get full ownership.

- Common for: Married couples, family members, business partners wanting automatic transfer.

- Downside: Cannot will your share to heirs; creditors of any joint tenant can claim against the property.

- Key Feature: Each owner has a separate, undivided interest which can be unequal (e.g., 70% / 30%).

- Survivorship Right: ❌ No — each owner’s share passes to their heirs, not automatically to co-owners.

- Best for: Partners, investors, or family members who want to leave their interest to heirs.

- Flexible: Owners can sell or will their share separately.

- Downside: Creditors of any co-owner can force sale of that owner’s share.

- Key Feature: Property acquired during marriage is presumed community property (owned equally).

- With Right of Survivorship Option: Some states allow this, so surviving spouse gets full ownership automatically.

- Tax Advantage: Full step-up in basis upon death of one spouse.

- Best for: Married couples in community property states.

- Only for: Married couples (or registered domestic partners in some states).

- Survivorship: ✅ Yes — surviving spouse gets full ownership automatically.

- Protection: Creditors of one spouse cannot force sale.

- Only in: Some states (not California).

- Best for: Married couples wanting survivorship and creditor protection.

- Held by: Living trust or other types of trusts.

- Purpose: Avoid probate, maintain privacy, estate planning.

- Survivorship: As defined by trust terms.

- Best for: Estate planning, asset protection.

- If you want automatic transfer at death, use Joint Tenancy, Community Property with Right of Survivorship, or Tenancy by the Entirety.

- If you want your share to go to heirs, use Tenancy in Common or hold in Trust.

- Consult an attorney if mixing types of owners (e.g., business + spouse) or for estate planning.

- Married Couple in California ✅ Best option: Community Property with Right of Survivorship for tax advantage & simple transfer.

- Business Partners ✅ Best option: Tenancy in Common to allow selling or inheritance of shares.

- Parent & Adult Child ✅ If parent wants child to inherit automatically: Joint Tenancy (but this can have tax/gift consequences). ✅ If want inheritance via will or trust: Tenancy in Common or Trust.

2. What’s the difference between a will and a trust?

A will uses probate to distribute assets post‑death. A trust bypasses probate, offering privacy and faster transfers. We help you choose the best strategy.3. I already have a trust — do I still need a will?

Yes. A pour‑over will transfers leftover assets into your trust and lets you name guardians for minors.4. What happens if I die without a will or trust?

State law determines heirs, not your wishes. We help prevent this with proper planning.5. What is a power of attorney (POA)?

A POA lets a trusted person manage your finances or healthcare if you cannot. We help prepare both financial and medical POAs.6. Who should be my executor or trustee?

Choose someone trustworthy—family, friend, or professional. We can refer you to legal or fiduciary partners.7. Can I update my estate plan?

Yes. Review every 2–3 years or after major life events like marriage or property changes.8. How do property titles affect my plan?

Ownership titles determine how assets transfer. We help structure titles to streamline distribution.9. What are probate vs. non‑probate assets?

Probate assets go through court. Non‑probate (like trusts or joint titles) transfer directly. We minimize probate for you.10.Do I need an estate plan if I’m not wealthy?

Yes—everyone needs a plan. It protects healthcare wishes, assets, and legacy, no matter your net worth.💰 MORTGAGES, SECOND LOANS & HELOC

1 . How do I apply for a home mortgage (step‑by‑step)?

Step 1: Get pre‑approved — gather pay stubs, W‑2s or 1099s, bank statements, tax returns (2 years if self‑employed), ID. Step 2: Choose loan type (e.g., conventional, FHA, VA). Step 3: Submit full application — lenders verify income, assets, credit. Step 4: Get locked loan terms/rates. Schedule appraisal and inspections. Step 5: Finish underwriting — supply any extra documents. Step 6: Clear to close — sign closing docs, fund, record deed, get keys.2. What kinds of mortgages are available?

• Conventional Fixed‑Rate: Stable rate 15–30 years. • Adjustable‑Rate (ARM): Lower initial rate, adjusts later. • FHA: Low down payment, flexible credit. • VA: 0% down for qualified veterans. • USDA: Rural homes with low income. • Jumbo: For loans above conforming limits.3. What benefits do first‑time homebuyers get?

• Lower down payment FHA loans. • Potential grant or down‑payment programs. • Tax credits in some areas. • Ability to waive appraisal contingency if financed by our lenders.4. How much should I save for a down payment?

• FHA: ~3.5% • Conventional (no PMI): 20% ideal • VA/USDA: Potentially 0% down • Other options: 5%–10% with PMI5. What FICO score do I need for different loan types?

• Conventional: 620+ • FHA: 580+ (some as low as 500) • VA/USDA: Typically 620+ • Jumbo: 700+ usually recommended6. What is a second loan or HELOC and why use one?

A second mortgage or Home Equity Line of Credit (HELOC) lets you borrow against your home’s equity. • HELOC: Revolving line, draw as needed, interest-only payments, • Second Mortgage: Lump-sum fixed-rate loan. **Use cases:** Home upgrades, debt consolidation, emergency needs, investment. We’ll help you compare rates, terms, and tax implications.🔑 HOME-BUYERS FAQ

1. What’s the first step in buying a home?

Get pre‑approved for a mortgage. It defines your budget and shows sellers you’re serious. We’ll help connect you with lenders.2. How do I find the right home?

We assist with search plans and home tours, guided by a licensed agent familiar with your needs.3. What should I look for during a tour?

Check layout, condition, neighborhood, and potential repairs. We help you assess value.4. How do I make an offer?

We craft competitive offers with proper contingencies to protect you.5. What happens after acceptance?

Escrow opens, deposit paid, inspections and appraisal begin.6. What inspections are needed?

Standard checks include home, termite, roof, and sewer. We coordinate everything.7. What is an appraisal?

Lender assesses value. If low, we help negotiate or appeal the outcome.8. What does underwriting mean?

Lender verifies your documentation. We coordinate with you to satisfy requests.9. What’s the final walkthrough?

Final inspection to verify condition and repairs before closing.10.What is closing escrow?

You sign documents and get the keys once loan funds and deed are recorded.🏠 HOME-SELLERS FAQ

1 . How do I start selling?

Book a consultation. We’ll evaluate and plan a full-service listing strategy.2. How do I pick an agent?

Look for experience, responsiveness, and local expertise. We offer start-to-finish support.3. What’s in the listing agreement?

It covers pricing, commission, terms, and duration. We explain it clearly.4. How do I prepare my home?

We help with staging, decluttering, repairs, and professional photos.5. How is the home marketed?

MLS, virtual tours, open houses, social media, email campaigns, and agent networking.6. How do I evaluate offers?

We help compare price, terms, and buyer strength to find your best match.7. What happens after accepting an offer?

Escrow opens. Buyer deposits funds, inspections and financing begin.8. What if inspections uncover issues?

We’ll negotiate repairs or credits while preserving your proceeds.9. Appraisal lower than sale price?

We can renegotiate terms, split the gap, or challenge the appraisal as needed.10.What must I do before closing?

Complete repairs, clear out, sign docs, and hand over keys and remotes.11. When do I get paid?

After closing and deed recording, escrow wires your net proceeds.Bonus Tip: Do I need to buy before I sell?

Not necessarily. We offer solutions like rent-backs, bridge loans, and contingent sales.🤝 ESCROW FAQ

1 . What is escrow?

Neutral party managing money, documents, and legal compliance during home transactions.2. When does escrow open?

Once the purchase contract is signed and earnest money is deposited.3. What does escrow do?

They hold funds, coordinate docs, verify compliance, and prepare for closing.4. Who does escrow represent?

No one—they remain impartial and follow both parties’ and lender’s instructions.5. What if something changes?

Escrow pauses until confirmed instructions are received. We help manage any modifications.6. What’s in final escrow paperwork?

Closing Disclosure, deed, loan docs, and signing instructions for buyer and seller.7. When do I sign?

1–5 days before closing. In-office, mobile notary, or online options available.8. When does escrow close?

When funds are received, documents are signed, and deeds are recorded. Buyer gets keys, seller gets paid.9. How long does escrow take?

Typically 21–30 days. Our team tracks each step to keep things on schedule.Bonus Tip: Who chooses the escrow company?

Usually the seller (in California), but it's flexible. We work with experienced escrow providers.Have you ever considered what will happen to your assets if you're no longer here one day? Without a clear plan, your entire estate could fall into the wrong hands or be tied up in a complicated legal process. Wills and Trusts are two legal tools that can help you answer this question.

Many people often confuse these two concepts or don't know which one to choose. Below is a detailed explanation of each to help you make the best decision for your personal circumstances.

1. What is a "Will"?

A Will, also known as a last will and testament, is a legal document that outlines how you want your assets to be distributed after you pass away.

In a Will, you can designate:

- Beneficiaries: The people who will receive your assets (e.g., children, spouse, relatives...).

- Executor: The person responsible for carrying out your wishes.

- Guardian: The person who will care for your minor children (if applicable).

After you pass away, your Will must go through a court process called Probate Court to verify its legality. This is a mandatory procedure that can take anywhere from a few months to several years and comes with legal and court fees. If there are disputes among beneficiaries, this process can become significantly more expensive and time-consuming.

Advantages of a Will:

- Simple and low-cost: Creating a Will is relatively easy and less expensive than a Trust.

- Guardian appointment: You can legally appoint a guardian for your children.

- Suitable for simple estates: This is a good option for those with straightforward and uncomplicated assets.

Disadvantages of a Will:

- Goes through Probate Court: The court process is very time-consuming, expensive, and lacks privacy.

- Public information: Your asset and beneficiary information becomes public record in court files.

- No effect while living: A Will only takes effect after your death.

2. What is a Trust?

A Trust is a more complex legal agreement. It involves you (the creator of the Trust, also known as the Grantor) transferring ownership of your assets to a third party (the Trust manager, also known as the Trustee) to manage and distribute them to the beneficiaries according to the conditions you set beforehand.

You can appoint yourself as the Trustee while you are alive to manage your assets directly. After you pass away, the person you designated will take over as Trustee and distribute the assets according to your instructions. Since the Trustee directly manages the assets, you need to choose someone you can truly rely on.

Trusts are typically divided into two types:

- Revocable Trust: You can change, amend, or revoke it while you are still alive.

- Irrevocable Trust: Once established, you cannot change or revoke it without the consent of all parties involved.

You can think of a Trust as a "safe deposit box" where you place all of your assets, including your home, car, insurance, investment accounts, etc. When assets are put into the Trust, legally, the "safe deposit box" itself becomes the owner, not you. This allows assets to be transferred directly to beneficiaries after your death without the need for the cumbersome Probate Court process.

Advantages of a Trust:

- Avoids Probate Court: This is the biggest advantage, saving time, money, and legal hassle.

- Information privacy: Information about your assets and beneficiaries is kept private.

- Effective asset management: You can set detailed conditions for asset distribution, such as providing funds only when a beneficiary reaches a certain age or graduates from college.

- Effective while living: A Trust is effective as soon as it is established, allowing for asset management even if you become incapacitated.

Disadvantages of a Trust:

- Complex and costly upfront: Creating a Trust is more complicated and expensive than a Will.

- Requires careful management: You need to manage the assets within the Trust carefully to ensure its effectiveness.

- Ineffective if improperly set up: If the Trust is not created or funded correctly, it may not function as intended.

Should You Choose a WILL or a TRUST?

In summary, a Will is suitable for those with simple estates who want to save on initial setup costs. In contrast, a Trust is the optimal choice if you want better asset protection, greater privacy, and, most importantly, to avoid the complicated Probate Court process.

The choice between a Will and a Trust depends entirely on your personal circumstances and financial goals. You should consult with an attorney to create the plan that is best for you.

Identity theft is a serious threat. Scammers can steal your personal information to open credit cards, take out loans, or start phone contracts in your name. The worst part is, you might not even know about it until the unpaid debts are sent to collection companies. By that point, your credit score could already be severely damaged, leaving you to spend significant time, effort, and money to fix the damage. Some people even get sued for debts they never incurred.

5 Things to Do When Your Identity Is Stolen

If you discover your identity has been stolen, take these five immediate steps:

Report it to the FTC (Federal Trade Commission): The FTC provides detailed guidance on recovery and offers useful resources, including necessary forms. You can file a report on their website: https://reportfraud.ftc.gov.

File a police report: Most cities allow you to file a report online. Simply search on Google for "Report identity theft" along with the name of your city.

Contact affected companies: If you know which credit card companies, banks, or phone companies the thief used to open accounts, contact them directly. Report the identity theft and ask them to close the fraudulent accounts immediately.

Request your credit reports: Contact the three major credit bureaus—Equifax, TransUnion, and Experian—and request your latest credit reports. You are entitled to a free report from each company once a year. Review the reports carefully. If you find any loans or accounts that aren't yours, report them immediately and demand an investigation and removal from your report.

Freeze your credit file immediately: This is the most crucial step, whether your identity has already been stolen or not. A credit freeze protects you from future fraud.

What is a Credit Freeze?

A credit freeze means you block credit reporting agencies from sharing your credit report with anyone. If a scammer gets hold of your information and tries to apply for a loan or open a credit card, the application will be automatically rejected because the system can't access your credit report. This is a powerful protective measure and will not negatively impact your credit score at all.

When you need to apply for a credit card, a loan to buy a house, or a car, you can temporarily unfreeze your credit online for the specific lender to check your file. You are in complete control.

Here are the websites for the three major credit bureaus where you can freeze your credit:

Experian: https://www.experian.com/

TransUnion: https://www.transunion.com

Equifax: https://www.equifax.com

A credit freeze is a simple and effective way to take control of your financial security. Have you ever considered freezing your credit?

Building a good credit score is essential for many financial goals, from getting a loan to renting an apartment. The common wisdom is simple: use your credit card and pay your bills on time. While that's absolutely true, the real challenge for many people is getting that first credit card.

Here are two effective ways to get started.

Method 1: Become an Authorized User

If you have a relative or a trusted friend with good credit, you can ask them to add you as an authorized user on one of their credit card accounts.

How it works: If they agree, the bank will issue a credit card in your name.

Benefits: You get a card and your credit history will be linked to the primary account holder’s good credit behavior, which can help you build your own credit history.

Important consideration: Legally, the primary account holder is responsible for all debt on the card. If you can't pay, they will have to.

Tip for parents: You can add your children as authorized users. By the time they turn 18, they may already have a solid credit history.

Method 2: Get a Secured Credit Card

If you don’t have a family member or friend to add you as an authorized user, a secured credit card is a great alternative.

How it works: You provide a cash deposit to the bank (e.g., $500), and the bank issues you a credit card with a credit limit equal to that deposit (in this case, $500).

Building trust: After you use the card responsibly and make timely payments for 6 to 12 months, the bank will often convert it to a regular, unsecured card and return your initial deposit.

Why it works: This method minimizes the risk for the bank, making it a perfect tool for building credit from scratch.

Using Your First Credit Card to Build Your Score

Once you have your first credit card, here’s what you need to do to build a strong credit history:

Use it for small, necessary expenses. Don't use your card for everything. Stick to essential purchases like groceries and gas, as these are easy to track and pay off.

Pay your bill on time, every month. This is the most crucial step. Aim to pay your balance in full every month to avoid paying interest.

Keep your credit utilization low. This means you should not use more than 30% of your credit limit. For example, if your limit is $500, try to keep your balance under $150.

Wait before applying for a new card. After about 6 to 12 months of responsible use, your credit score will improve. At this point, you can consider applying for a second, unsecured credit card.

Tips to Keep in Mind

Avoid applying for multiple cards at once. Every time you apply for credit, it results in a "hard inquiry" on your credit report, which can cause your score to drop by a few points. It's best to limit applications to one new card per year.

Never spend money you don’t have. A credit card should be a tool for building credit, not for going into debt. Always have enough cash on hand to pay your balance in full.

Pay off your balance within 30 days. If you don't pay your full statement balance by the due date, you will be charged interest daily.

Don't close old credit accounts. Keeping old accounts open, especially if they have no annual fee, helps your credit score by increasing your available credit and improving the average age of your accounts. Use the card every now and then to keep the account active.

Mortgage Questions

Most lenders require a credit score of at least 620 for a conventional loan, but FHA loans may be available with scores as low as 580. Higher credit scores often qualify for better interest rates.

The required down payment varies by loan type:

- Conventional Loan: Typically 5-20%

- FHA Loan: As low as 3.5%

- VA & USDA Loans: 0% (for eligible buyers)

Common mortgage options include:

- Fixed-Rate Mortgage: Stable interest rate for the loan term.

- Adjustable-Rate Mortgage (ARM): Interest rate changes periodically.

- FHA Loan: Lower down payment, government-backed.

- VA Loan: Exclusive to veterans and active military.

- Jumbo Loan: For high-value properties exceeding loan limits.

To get pre-approved, you’ll need to submit financial documents like proof of income, credit history, employment details, and bank statements to a lender. Pre-approval helps you understand your budget and strengthens your offer when buying a home.

Your interest rate depends on:

- Credit score & financial history

- Loan amount & term length

- Down payment size

- Current market conditions

- Debt-to-income (DTI) ratio

Yes! Refinancing allows homeowners to secure a lower interest rate, reduce monthly payments, or shorten their loan term. It’s a great option if rates have dropped or if your financial situation has improved.

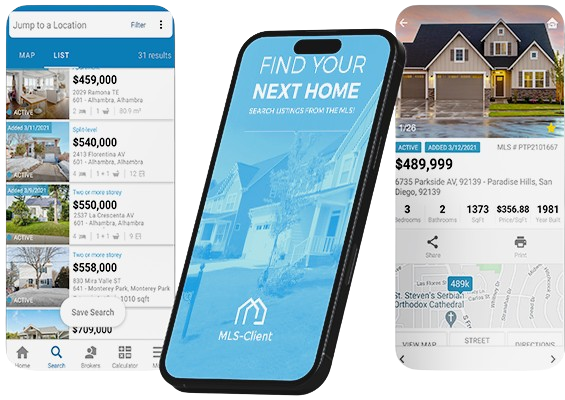

DOWNLOAD the FREE MLS APP BELOW to SEARCH NEW LISTINGS in REAL-TIME

ACCESS THE LATEST MLS LISTINGS

Download the MLS-CLIENT App!

If you’re looking for the most current and updated property listings, our MLS-CLIENT app gives you direct access to the Multiple-Listing-Services (MLS) in real-time! This app provides you with an easy-to-use platform to search for properties, view details, and stay informed about new listings as they hit the market.

How to Get Started:

- Click this direct link https://mls-client.com/DD45E58D to download the MLS-CLIENT app onto your computer or mobile phone (IOS or Android)

- The app is 100% FREE to download and use.

- If asked, please enter the access code DD45E58D to download and unlock full property search capabilities.

With the MLS-CLIENT app, you’ll have up-to-date real estate listings at your fingertips anytime, anywhere. Don’t miss out on your dream home—download the app today and start searching for your new home!

Download Now: https://mls-client.com/DD45E58D

For any questions or assistance, feel free to contact us: info@Siriusfinancialrealty.com